Gambling, Drugs and Alcohol

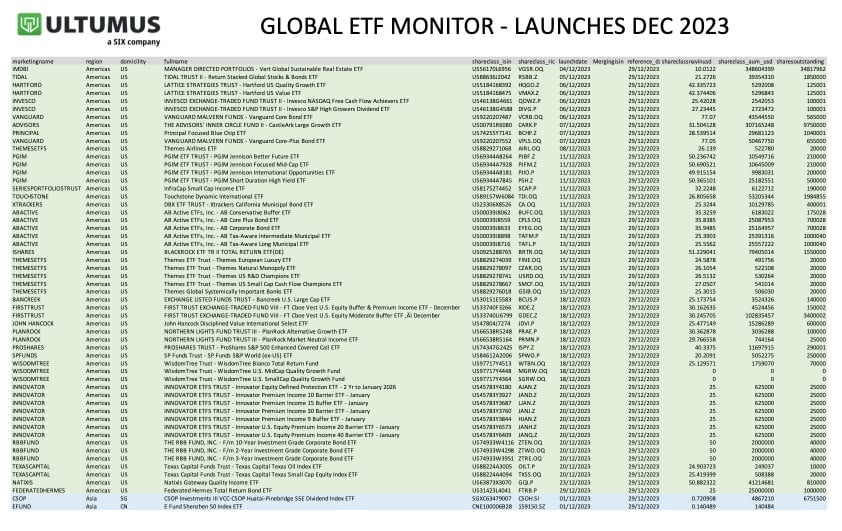

Lets see how many firewalls block this email.. this ETF was launched in early Dec, but I missed it as i was out skiing, but i felt compelled to cover it....

Sin stock ETF with shortest name ever

ETF newcomer the BAD Investment Company has launched an ETF that buys all the companies your parents tell you not to.

BAD ETF (BAD) – which, at just six letters long, has the shortest name of any ETF in the world – invest in what are called “sin stocks”. These are companies in gambling, alcohol, marijuana and drugs.

Sinful companies are identified by reading their financial statements, media reports, and other research.

Examples of companies included in the fund are casino operators Wynn Resorts and Las Vegas Sands. Alcohol companies like Diageo and Corrs. As well as plain old pharmaceutical companies like Abbvie and Pfizer.

The index, called the EQM BAD Index, is equally weighted and open to large global companies.

This is not the first sin stock ETF in the United States. AdvisorShares Vice ETF (VICE) pursues a similar strategy.

The fund charges 0.75%.

Bernie’s commentary – BAD idea

The thesis behind this fund is as follows: ESG funds are becoming more common. As a matter of practice, ESG funds exclude companies like casinos and alcohol businesses. But… casinos, drug makers, alcohol companies are highly profitable. And that ESG investors avoid them can make them cheap—and especially cheap given the profit they make. This aversion of ESG investors thus creates an opportunity for other investors with fewer ethical misgivings.

While the thesis makes sense, there’s a few things I don’t quite agree with:

- The fund name. It’s nice to have the shortest name ever. And I too hate it when long fund names distort my excel spreadsheets. But “BAD ETF” – without even the word “the” in front – kind of sounds like you’re speaking to a dog. “Bad dog. Bad boy. Bad ETF.”

- Why are big pharmaceutical companies in this? Who thinks Pfizer is a sin stock? Excluding these businesses is not standard at all for mainstream ESG frameworks.

- Alcohol companies are in structural decline. Their stock prices aren’t necessarily cheap. The upcoming generations – generation Z and millennials – are drinking significantly less. There has been a lot of social commentary around this, much of which has praised the young for their discipline. But in my view their break with alcohol likely has darker roots. Drinking is a social activity—what you do with your friends and family. Millennials have fewer friends (both platonic and lovers) and family sizes are shrinking. And while millennials are less addicted to alcohol, they are more addicted to social media and electronic devices, does our definition of sin need to expand to include Facebook.

What Stocks are considered Sin Stocks?

Sin stocks can include gambling and betting, adult entertainment/pornography, alcohol, tobacco, recreational marijuana, and some types of weapons. These are all examples of industrial sectors that can be excluded by ESG policies and/or religious guidelines for investing, which might also exclude areas such as abortion or contraception related drugs, devices, equipment or treatments. Meanwhile, Islamic Shariah investing guidelines could exclude leveraged companies, which are above certain debt thresholds, in any industry.

On marijuana, it may be nuanced. Pure medical/therapeutic marijuana might not be a sin stock but recreational marijuana could be (and may also be illegal to invest in for some countries).

On weapons, controversial weapons, such as the land mines and cluster bombs being used in the Russia/Ukraine war, might be sin stocks but other more conventional weapons may not be.

More controversially, certain drug companies associated with scandals such as opioids might be excluded.

The rise of ESG investing has led to some additional sectors, such as oil and gas, and coal, being considered as “sin” stocks based on their contribution to global warming. Here there are also nuances with coal being perceived as a very “dirty” fuel while natural gas may be seen as the “cleanest” fossil fuel. Within the oil space distinctions can also be made between oil coming from tar sands, shale oil and other sources of oil.

Are Sin stocks a good investment?

Portfolio managers, financial advisors, and individual investors who make their own decisions, need to form a view on the valuation and growth prospects of various “sin” sectors and individual companies, to work out the risk and return profile. Whether they are good investment will vary between individual investors, pension funds, insurance companies and so on, depending on their investment mandate, return targets, risk tolerance and other factors. That said, it is likely that many well diversified equity funds and ETFs will include some stocks that might be classified as “sin” and certainly any broad US or global index tracker based on indices such as the S&P 500 or the MSCI World, will contain some “sin” stocks.

Do sin stocks outperform?

Many studies suggest that sin stocks have historically outperformed over long periods, but not necessarily in every calendar year. For instance in 2023 AI and technology were clearly leading the markets and outperforming all other sectors. In contrast 2022 was a very different story where energy stocks (sometimes classified as “sin”) were some of the only sectors to produce positive performance. These sorts of studies are naturally going to be quite sensitive to the chosen start date and end date, and also the benchmark. The US equity market has a heavy weighting in technology that has been the best sector for the past decade, whereas in European markets with much less technology it is easier for a possible ”sin” stock such as a luxury goods maker also producing alcohol to outperform the average.

What is the difference between ESG and sin stocks?

Some types of ESG policies that use negative screening or exclusions, will not invest in certain sin stocks, usually based on some minimum threshold of revenues coming from a sin sector. However ESG is a much broader subject than just excluding companies or industries, and some ESG policies and approaches might not have any exclusions at all. Some ESG strategies also want to identify and overweight companies that make a positive impact on measures such as the UN Sustainable Development Goals, which can sometimes be called “impact investing”. And some more active ESG approaches work constructively with all sorts of companies to try and improve their ESG performance through engagement with boards and management, voting at company meetings, and proposing issues, such as climate policies, which might be added to the agenda of company meetings.